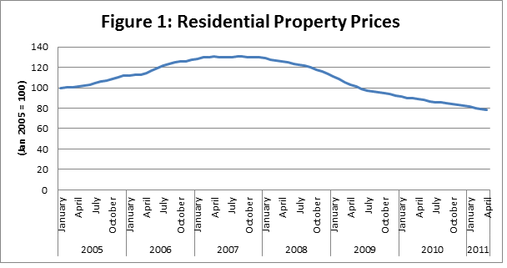

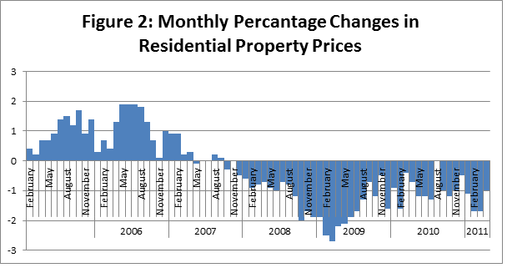

The latest figures from the CSO show that house prices have continued to fall in May 2011. So far, in the year to May, prices have fallen by 12.2%. In May itself, prices fell by 1.2%, up from a fall of 1% in April. House Prices in Dublin are almost 46% lower than at their highest level in early 2007. Apartments in Dublin are 53% lower than they were in February 2007.

RSS Feed

RSS Feed