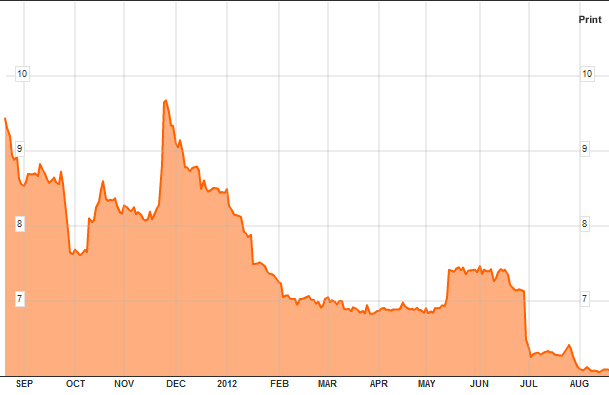

Ireland's 9 year bond yield has dropped below 6% for the first time since October 2010. Looking at the graph below we can see this is reflective of a generally downward trend over the past few weeks. Rates have fallen from a high of over 9.5% in December 2011 and while they rose slightly in June they have returned to their downward trend. This reduction in the cost of borrowing will be welcomed by Government as it is viewed as a measure of the credibility international investors view Ireland with. This follows the state raising €5 billion on the bond market last month.

RSS Feed

RSS Feed