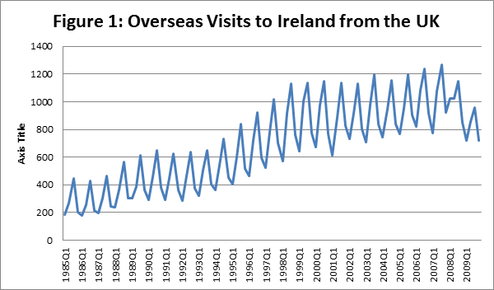

In light of the visit by the Queen to Ireland it is interesting to consider the interconnectedness of the Irish economy and the economy of the United Kingdom (UK). In terms of visits to Ireland by people from the UK we can see in Figure 1 that this has been increasing steadily from the mid-1980s (with the usual seasonal variation associated with tourism). However, must likely due to the recession this upward trend has been slightly abated since 2008.

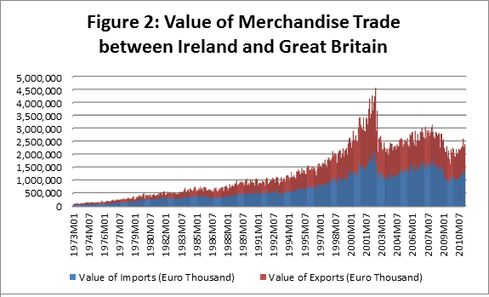

In terms of merchandise trade, Ireland is also becoming more interconnected with the UK (see Figure 2). Since the 1970s our trade with the UK has increased exponentially, peaking during the end of the 1990s at the height of the Celtic Tiger and declining slightly during the construction bubble phase of the economy. However, despite this decline in the latter part of the last decade, the UK remains Ireland’s largest export market.

These two graphs are just an example of the interconnectedness of Ireland with our nearest neighbour and show how important the UK economy is for the Irish economy as a customer base for our tourism industry and also as a destination for our exports.

RSS Feed

RSS Feed