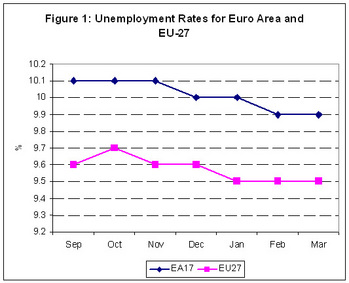

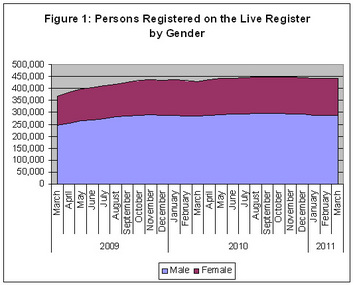

Euro level unemployment is at a rate of 9.9% in March 2011. This is down from 10.1% in March of 2011. Comparably, the EU-27 unemployment rate has fallen from 9.7% to 9.5% over the same time period. This decline in unemployment figures, however small, is a positive event. As shown in Figure 1 the downward pattern has been prevalent since September of last year.

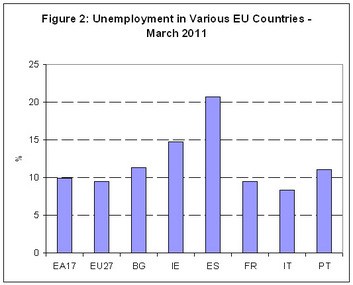

Comparing Ireland to some of our neighbours we are faring particularly poorly when it comes to unemployment figures. This is highlighted by Figure 2 which presents Ireland and a number of our European counterparts for whom data is available for March 2011. We can see that with the exception of Spain (ES) Ireland possesses one of the highest unemployment rates in Europe. As Ireland was coming from one of the lowest levels of unemployment in Europe in 2007, this highlights Ireland’s dramatic fall.

RSS Feed

RSS Feed