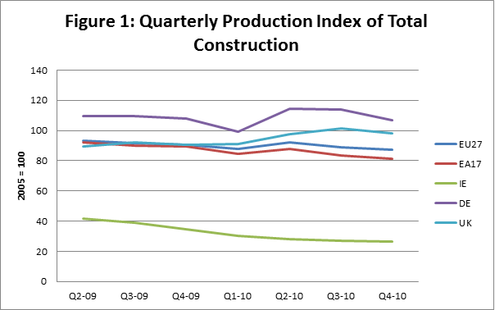

The latest figures released from Eurostat indicate that Ireland’s construction demise has been among the worst of all the EU-27 countries. Figure 1 shows this decline compared to the European average and some other selected countries. Using 2005 as the base year of 100, Ireland’s construction output has fall by 73%. This fall is far in excess of the European average which has seen a fall of only 13%. And while the Euro Area has been more adversely effected than the rest of Europe this has only fallen by 18%. Germany’s construction output is actually higher in Q4 2010 than in was in 2005 while the UK has seen improvements in construction output throughout 2010.

These figures indicate that while Ireland is not the only country to be adversely effected through a collapse in the construction industry, we appear to have suffered more than most. Perhaps indicating the extent to which the construction industry in Ireland had overheated.

RSS Feed

RSS Feed