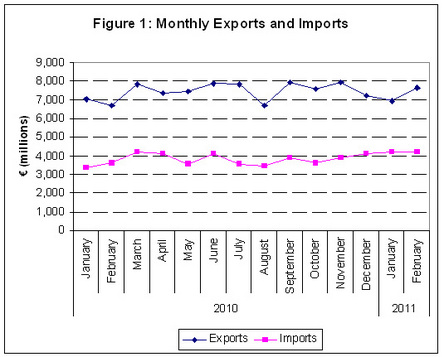

Exports have risen in February of 2011 increasing by 11%. However, over the same time period imports have actually decreased by 3%.

It can be seen in Figure 1 that exports in February of 2011 are substantial higher than they were in 2010. This indicates a strong performance by Irish exporters, and is a turnaround from a dip in exports in January 2011. This slight dip in exports in January 2011, coupled with an increase in imports, resulted in Ireland’s trade surplus decreasing slightly. However, due to rising exports, this has trend has been reversed and in February Ireland’s terms of trade surplus increased to €3.8 billion.

RSS Feed

RSS Feed