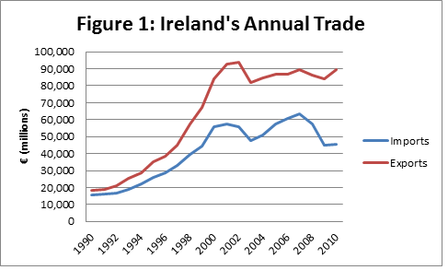

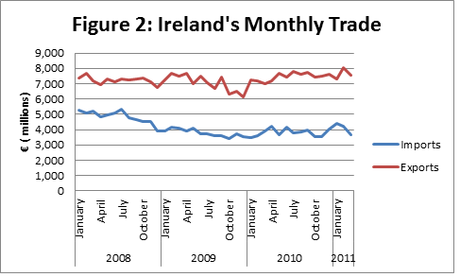

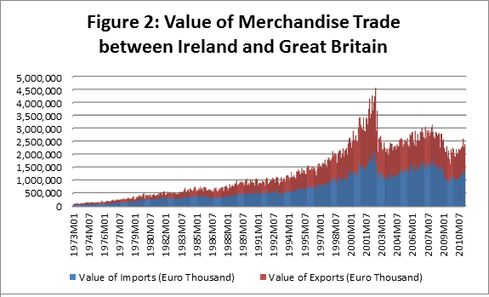

Ireland’s exports have decreased slightly in March 2011 compared to February, but the trade surplus has increased following a decline in imports. Figure 1 shows how Ireland’s trade surplus has been historically widening since the Celtic Tiger period of economic growth from the early 1990s onwards.

This has continued to widen in 2011 as shown in Figure 2. The fall of 6% in monthly exports between February 2011 and March 2011 was offset by a fall in imports of 15% over the same time horizon. This resulted in a 3% increase in Ireland’s trade surplus in March 2011.

RSS Feed

RSS Feed