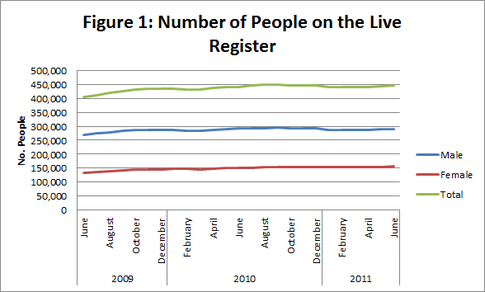

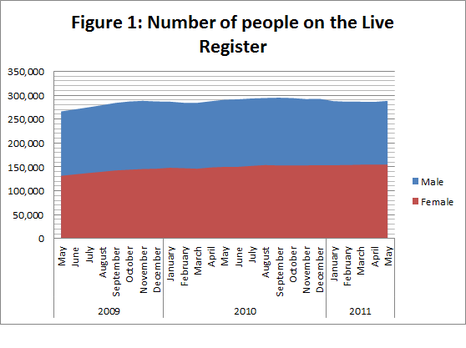

June has seen a slight increase in the number of people on the live register. The total increase was 2,900 people, which is approximately an increase of 0.7%. This is highlighted in Figure 1, with both the number of women and men signing onto the live register increasing.

RSS Feed

RSS Feed